Published in Business Today, Astro Awani, New Straits Times & Focus Malaysia, image by Business Today.

Although the flexibility offered by the gig economy has encouraged more Malaysians to be self-employed during recent years, the Covid-19 pandemic reveals the vulnerability of the social protection system in Malaysia.

With various lockdown measures introduced in the country, more self-employed have been struggling to sustain their business operations.

As many businesses were forced to close temporarily when the Movement Control Order (MCO) commenced in early March last year, the Department of Statistics Malaysia (DOSM) revealed in their survey findings that 46.6% of the self-employed lost their jobs. Only 5% of self-employed in Malaysia had enough savings to last for at least three months.

Unlike a typical employee who earns a consistent monthly salary, self-employed individuals have to find numerous sources of income to cope with the rising cost of living.

Traditional employees also could save more as they are eligible to receive fixed bonuses at the end of the year. In contrast, a self-employed person has to put in more effort to maintain their income and savings.

As the earnings among the self-employed can be highly variable, they may not have the ability to commit to annual premiums or may not have enough credit ratings to gain access to loans. When they could not access any loan from any formal financial institutions, their last resort would be to borrow money from their family and friends. Only then, at least, they could cover the monthly rental, utilities and overhead related expenses.

In addition, the self-employed may be forced to continue working in the case of sickness as they are not entitled to any sickness benefits.

Therefore, being self-employed is known as a vulnerable type of employment. The self-employed are either not covered by work-related social protection (i.e., health insurance and pension funds) or entitled to certain employment benefits (i.e., paid vacations and sick leave).

According to the DOSM, there are four types of employment status in the country:

- Employees or those who work for others for pay;

- Own account workers or self-employed;

- Unpaid family workers or those working in a family business without pay; and

- Employers who operate businesses with at least one worker.

As of the second quarter (Q2) of 2021, the self-employed are now the second largest group in the Malaysian workforce. Out of a total of 15.21 million working adults, 17.2% or 2.61 million are self-employed.

Based on the DOSM’s definition, the self-employed refers to a person who operates his or her own farm, business or trade without employing any paid workers assisting in the conduct of the enterprise. E-hailing drivers and delivery riders, freelancers and food stall owners are also known as self-employed individuals.

Unlike standard employees who have fixed working hours to comply with, self-employed are the ones who tend to have non-regular working hours. They even have to work during night time or weekends.

Micro and small brick and mortar businesses, in particular, are relatively more vulnerable to economic shocks as they do not have a strong cash flow compared to large enterprises.

E-hailing drivers, delivery riders and food stall owners feel the pinch of the pandemic even more as they do not have the luxury to work from home. As they require physical presence to perform their job, the movement restrictions arising from the Covid-19 pandemic have constrained their ability to go out and earn daily wages to survive.

Prolonged lockdown measures also led to more Malaysians who found it difficult to put food on the table. Some of them had to raise white flags to seek help due to the loss of jobs and income.

Even though the Malaysian government has introduced numerous stimulus packages for the self-employed to make ends meet, the employment retention measures tend to be less effective due to a significant proportion of self-employed in the country.

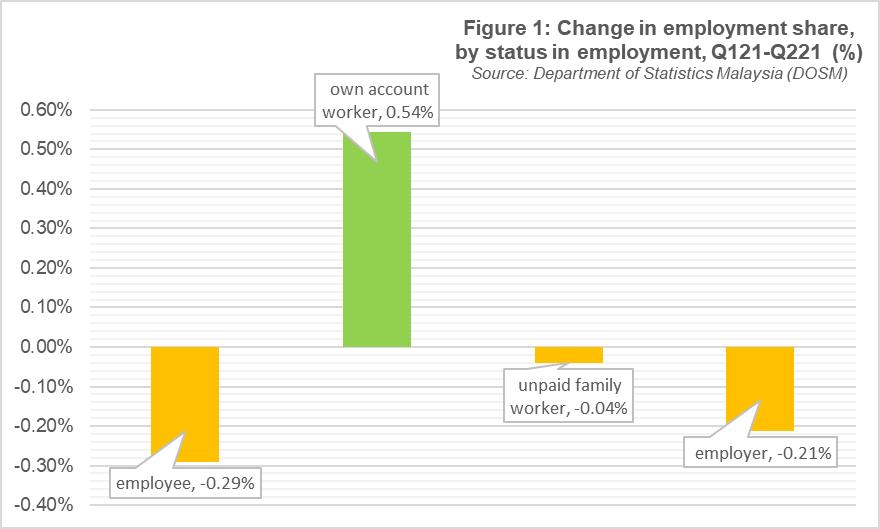

Although the total number of employed persons has declined from 15.23 million to 15.21 million, Figure 1 shows that the employment share for own account worker/self-employed between Q121 to Q221 has generally risen with other forms of employment declining.

The stimulus package measures that specifically cater for self-employed workers are a one-off payment for full-time e-hailing drivers and taxi drivers aside from the micro-credit for own-operators of businesses. The one-off assistance only covers a particular group of self-employed. On the other hand, the micro-credit initiative is not direct financial assistance but more towards reducing associated operational costs.

Moreover, the design of the current social security and insurance scheme provides protection only for traditional employees who are within Social Security Organisation (SOCSO)’s and Employees Provident Fund (EPF)’s database. Although SOCSO plans to address the issue associated with the Self-Employment Social Security Scheme (SESS), the programme remains undersubscribed among self-employed individuals. Aside from the Self-Employment Insurance System (EIS), the i-Lestari is also not applicable to the self-employed.

As the verification to determine eligibility for Bantuan Sara Hidup (BSH) is purely based on the Inland Revenue Board of Malaysia (LHDN)’s data, again, the self-employed are the vulnerable ones who are not include in the welfare distribution system.

As a result, the only support for the self-employed would be the one-off cash payment from the Bantuan Prihatin Nasional (BPN) and the annual BSH. If the self-employed do not register their businesses, they are also not qualified to receive financial assistance specifically for Small and Medium Enterprises (SMEs).

In contrast, traditional employees not only could benefit from the i-Lestari provision and the BPN, but they also could receive assistance from the Employment Retention Programme (ERP), EIS and Wage Subsidy Programme (WSP).

Therefore, to enhance the social protection coverage among the self-employed, EMIR Research has the following policy recommendations for the current administration to consider:

- Address the gaps between the typical employees and self-employed in both social security and insurance programmes. For instance, the government could extend the benefits of ERP, WSP, utility bill discounts and special tax deductions for rental reductions among the self-employed.

Monthly assistance that is similar to what traditional employees are receiving is worth considering as it would increase the resilience of the labour force in addressing future economic shocks;

2. Enhance the labour market statistics landscape to be more comprehensive, and granular, and updating data on developments in the labour market is the key to producing quality data analysis for Malaysia to design people-centric public policies, especially among the self-employed;

3. Deliver holistic assessments on the current social security and insurance programmes with different government agencies (i.e., SOCSO and EPF), improving social welfare among the self-employed while ensuring all self-employed are protected during retirement;

4. Eliminate the bureaucratic processes and delays that prevent self-employed from accessing the benefits they urgently require; and

5.Amend both Self-Employment Social Security Act 2017 (Act 789) and Employment Insurance System Act 2017 (Act 800) to protect among self-employed in the event of work-related injuries or diseases or during the loss of employment.

Instead of introducing a general policy that purely focuses on the dynamic relations between employer and employee, now comes the ample opportunity for the Malaysian government to establish social protection floor for self-employed weathering through the public health crisis.

Amanda Yeo is Research Analyst at EMIR Research, an independent think tank focused on strategic policy recommendations based on rigorous research.